Where Have All the Good Accommodation Property Deals Gone?

I’m sharing this because Instagram can make accommodation look so easy.

You see the finished cabins, the dreamy photos, the “booked out” posts, and suddenly it feels like everyone is doing it. There are new stays popping up everywhere. And I swear most people I know have had that moment of romanticising it, thinking, “Maybe we should do this too.”

Then if you haven’t, it’s easy to start beating yourself up.

So here’s the hard truth I wish more people said out loud.

A lot of what looks effortless online is only effortless because of what you don’t see behind the scenes.

Many people making it look easy have one of these advantages:

they have the cash and don’t need a big mortgage

they already own the land and adding cabins is a bonus layer

they bought years ago, so their holding costs are completely different

they can build slowly without a repayment clock ticking in the background

And that changes everything.

This isn’t a “don’t do it” post.

It’s a “stop comparing yourself to someone else’s setup” post.

My golden rule

For me, I stick to looking at property within 2 to 3 hours of a major city.

Once you go further out, last-minute escape bookings drop, staffing gets harder, and the risk goes up. I’m not saying remote areas can’t work. I’m saying you need a different appetite for uncertainty.

The part that changes the whole game: the mortgage

The thing I’ve learned is simple.

A property can look like a “good deal”… until you add debt.

Because the bank doesn’t care how gorgeous it will be after the renovation.

And in a lot of locations now, $2 million doesn’t even buy what people truly want to stay in. So let’s talk about what happens when you’re carrying something like a $3 million mortgage.

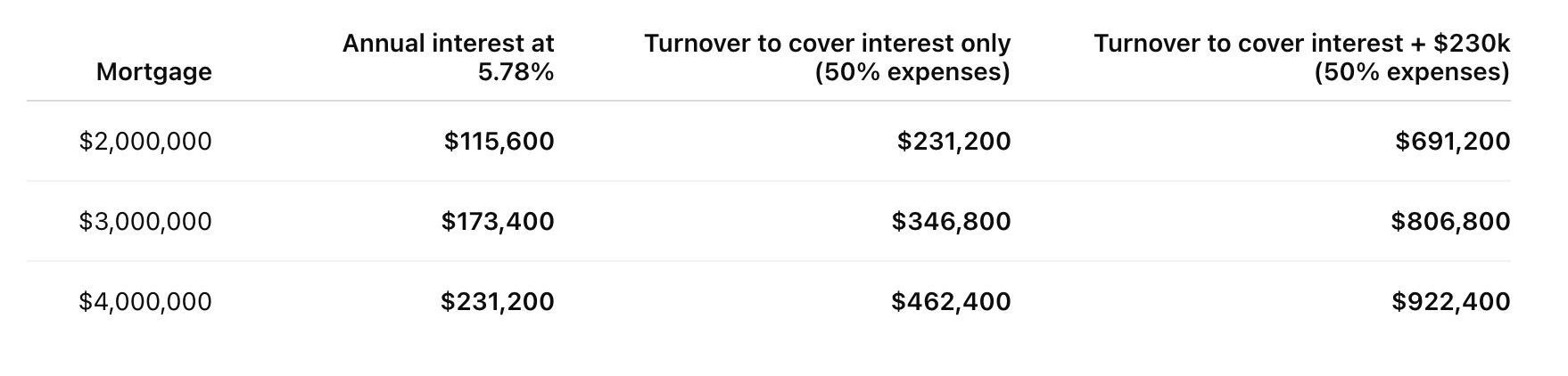

This is a simple, back-of-napkin example using a credible benchmark.

The Reserve Bank of Australia’s lenders’ rates table shows that in October 2025, the average rate for new investment interest-only loans was 5.78% p.a.

(Your actual rate may be different. This is just to illustrate the maths.)

The rule of thumb I use

Operating costs often chew up a big chunk of revenue. Cleaning, linen, maintenance, utilities, supplies, insurance, platform fees, management time.

My rough rule of thumb is:

Assume operating costs are around 50% of turnover.

So whatever you think you’ll make, cut it in half before you start dreaming.

The “magic number” you need to make it worth it

For me personally, if I’m taking on the stress and workload of running accommodation, I want:

$150k pay (otherwise it’s not worth the time)

$80k buffer every year (because something always happens)

So that’s $230k a year I want left over after operating costs, on top of covering the mortgage interest.

The numbers

Using a $3m mortgage and the 5.78% benchmark:

Annual interest = $3,000,000 × 0.0578 = $173,400

If operating costs are ~50%, then to cover that interest you need about double in turnover.

Then add my pay + buffer ($230k) to the “needs to be covered” side, and double that too.

Here’s the table:

The bit that hits you in the face

With a $3m mortgage, you’re looking at roughly $806,800 in annual turnover to cover:

interest at that benchmark rate

a $150k wage

an $80k buffer

assuming operating costs are about half

And that is why the “good deals” feel harder to find.

Because once you add debt, average accommodation does not work. It needs to be premium. It needs to be consistent. It needs to perform year after year.

A quick reality check on what that means

To gross $806,800 per year, a single property has to be either:

charge $2,763.01 per night with 80% occupancy rate year round.

or it needs multiple dwellings all charging high nightly rates.

This is why dated properties selling at premium prices make me nervous. You’re not just asking, “Can I renovate this?”

You’re asking, “Can this property realistically produce $800k a year, every year, without me losing my mind?”

Skip the Wage and Rely on Capital Gains

The idea:

You’re not trying to “earn a wage” from the property each year. You just want it to pay for itself, and you’re relying on capital growth over time.

What you still need the property to cover each year:

Operating costs (cleaning, linen, utilities, maintenance, insurance, fees)

Mortgage interest

An $80,000 buffer for the stuff that always happens

What that looks like with a $3m mortgage (example only):

Interest only at 5.78% = $173,400 interest per year

Add $80,000 buffer = $253,400 needed after expenses

If operating costs are roughly 50% of turnover, you need to gross about double that

Required turnover ≈ $506,800 per year

The catch:

This can work, but only if you can hold the property long enough for capital growth to show up, and you remember that stamp duty, selling costs, and capital gains tax can take a bite when you exit.

So where are the deals?

I don’t think deals are dead.

I think the old type of deal is rarer.

The deal used to be: buy dated, renovate, and the numbers naturally worked.

Now the deal has to be: buy something with genuine upside that the market hasn’t priced in yet.

And if you’ve looked at the numbers and thought, “That feels like a financial stress trap,” you’re not behind.

You’re just seeing what Instagram doesn’t show.

What I’m doing now

So for me, I’m not 100% sure what the next move is.

Right now, I’m sitting back and waiting. I’ll focus on my existing properties (Hyams Beach and the Orchard)

Not because I’ve given up on new deals, but because I refuse to force a deal that doesn’t make sense.

If dated places come down in value, that’s when the upside returns. That’s when you can buy something tired, transform it properly, and still have room in the numbers for a mortgage, the renovation, and the reality of running the business.

And yes, I’m always trying to think outside the box. I love an unconventional idea. I love a hidden gem. I love a “no one else sees it yet” moment.

But at the moment, I haven’t found an outside the box opportunity that stacks up on paper and feels right in real life.

So I’ll wait.

Because the right opportunity always shows up eventually. And when it does, I want to be ready, not financially stretched and stressed.